AI in Financial Infrastructure: Fraud, Compliance, Lending & Agentic AI [2026] - CoreFi

CoreFi · 13 min read

![AI in Financial Infrastructure: Fraud, Compliance, Lending & Agentic AI [2026] - CoreFi](/wp-content/uploads/2024/11/3.png)

Every fintech vendor's 2026 roadmap mentions "AI-powered" something. Very few can tell you what that actually means in production.

This article goes deep on four AI applications that are delivering real value in financial infrastructure today — not theoretical use cases, but systems running in production with measurable ROI. We'll cover the architecture, the data requirements, the regulatory constraints, and the honest limitations.

Application 1: Real-Time Fraud Detection

The Problem

Traditional rule-based fraud detection generates 95%+ false positives. Every false positive is a blocked legitimate customer, a support call, and eroding trust. Meanwhile, actual fraud gets more sophisticated — synthetic identities, account takeover via SIM swaps, and authorized push payment (APP) fraud now account for the majority of financial losses.

The AI Solution

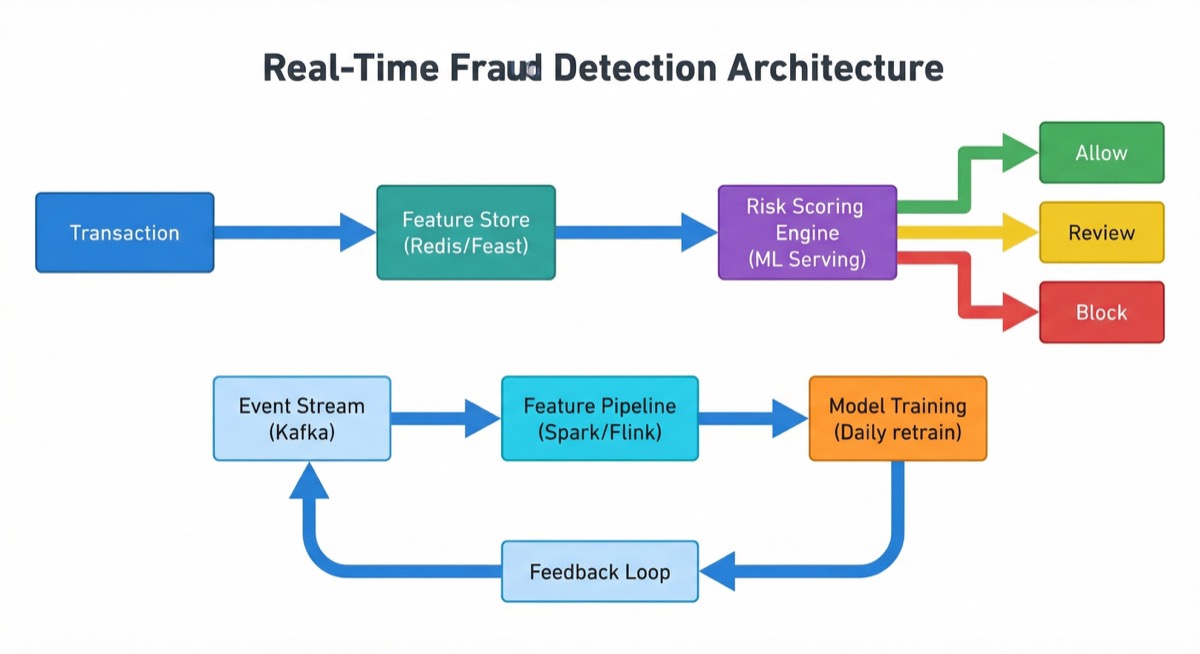

Modern fraud detection uses a layered ML approach:

Layer 1 — Behavioral Biometrics (Device & Session)

- Keystroke dynamics, mouse movement patterns, touch pressure

- Device fingerprinting and anomaly detection

- Session behavior modeling (time of day, navigation patterns, typical actions)

Layer 2 — Transaction Risk Scoring (Real-Time)

- Ensemble model combining gradient-boosted trees (XGBoost/LightGBM) for tabular features with neural networks for sequence patterns

- Features: amount, merchant category, location, velocity, device, time, counterparty history

- Sub-100ms inference latency required for payment authorization

Layer 3 — Network Analysis (Near Real-Time)

- Graph neural networks mapping relationships between accounts, devices, IPs, and merchants

- Identifies fraud rings and money mule networks

- Batch-updated every 5-15 minutes, used as features in Layer 2 scoring

Architecture Pattern

Data Requirements

- Minimum 6 months of labeled transaction data (fraud/not-fraud)

- Class imbalance is extreme: typically 0.1-0.3% fraud rate

- SMOTE and other oversampling techniques help but don't eliminate the cold start problem

- New entrants should start with rule-based systems augmented by vendor models, then train custom models once sufficient data accumulates

Measured ROI

| Metric | Before AI | After AI | Improvement |

|---|---|---|---|

| False positive rate | 95-98% | 40-60% | 50-60% reduction |

| Fraud detection rate | 60-70% | 85-95% | 25-35% improvement |

| Manual review volume | 100% of alerts | 20-30% of alerts | 70-80% reduction |

| Average detection time | Minutes-hours | <500ms | Real-time |

| Annual fraud losses | Baseline | -40-60% | Significant reduction |

For a mid-size fintech processing €500M/year, reducing fraud losses by 40% typically saves €500K-2M/year while simultaneously reducing the fraud ops team by 2-3 FTEs (€150-250K/year savings).

Regulatory Constraints

- Explainability: EU AI Act classifies credit scoring and fraud detection as "high-risk." Models must provide explanations for decisions that impact customers.

- Right to human review: Customers who are blocked or flagged must be able to request human review (GDPR Art. 22)

- Non-discrimination: Models must be tested for bias across protected characteristics

- Data retention: Transaction data used for model training falls under GDPR retention limits

Application 2: AML/Compliance Automation

The Problem

Financial institutions spend €50-200K/year per compliance FTE, and a mid-size firm typically needs 5-15 compliance staff. The vast majority of their time is spent on repetitive tasks: screening alerts, reviewing transactions, writing SARs, and checking sanctions lists.

The AI Solution

Intelligent Alert Triage:

- NLP models that read alert context and recommend dismiss/escalate/investigate

- Reduces Level 1 analyst workload by 60-80%

- Learning from analyst decisions to improve over time

Automated SAR Narrative Generation:

- Large Language Models (LLMs) that draft Suspicious Activity Reports from structured data

- Analyst reviews and edits (never fully automated — regulatory requirement)

- Reduces SAR writing time from 2-4 hours to 30-60 minutes

Dynamic Risk Scoring:

- Customer risk profiles that update in real-time based on transaction patterns

- Replaces static annual reviews with continuous monitoring

- Flags behavioral changes (sudden international transfers, new counterparties, unusual volumes)

Enhanced Due Diligence (EDD) Automation:

- Automated gathering of public information (company registries, UBO databases, adverse media)

- NLP-powered adverse media screening with relevance scoring

- Structured EDD reports generated automatically, reviewed by compliance officers

Measured ROI

| Metric | Impact | Annual Savings |

|---|---|---|

| Alert triage automation | 70% of L1 alerts auto-resolved | €150-300K (2-4 FTEs) |

| SAR writing assistance | 60% time reduction | €80-150K |

| Dynamic risk scoring | 50% fewer false positive EDD triggers | €50-100K |

| Adverse media screening | 80% reduction in manual searches | €40-80K |

| Total | €320-630K/year |

The Honest Limitations

- You can't fully automate compliance decisions. Regulators require human accountability. AI assists; humans decide.

- Model drift is real. Criminal typologies change. Models trained on last year's patterns miss this year's schemes. Monthly retraining is the minimum.

- Regulatory approval varies. Some NCAs embrace AI in compliance; others are skeptical. Check with your regulator before deploying.

Application 3: AI-Powered Credit Decisioning

The Problem

Traditional credit scoring relies on credit bureau data and manual underwriting rules. This excludes millions of creditworthy individuals (thin-file, immigrants, gig workers) and is too slow for modern lending products that promise instant decisions.

The AI Solution

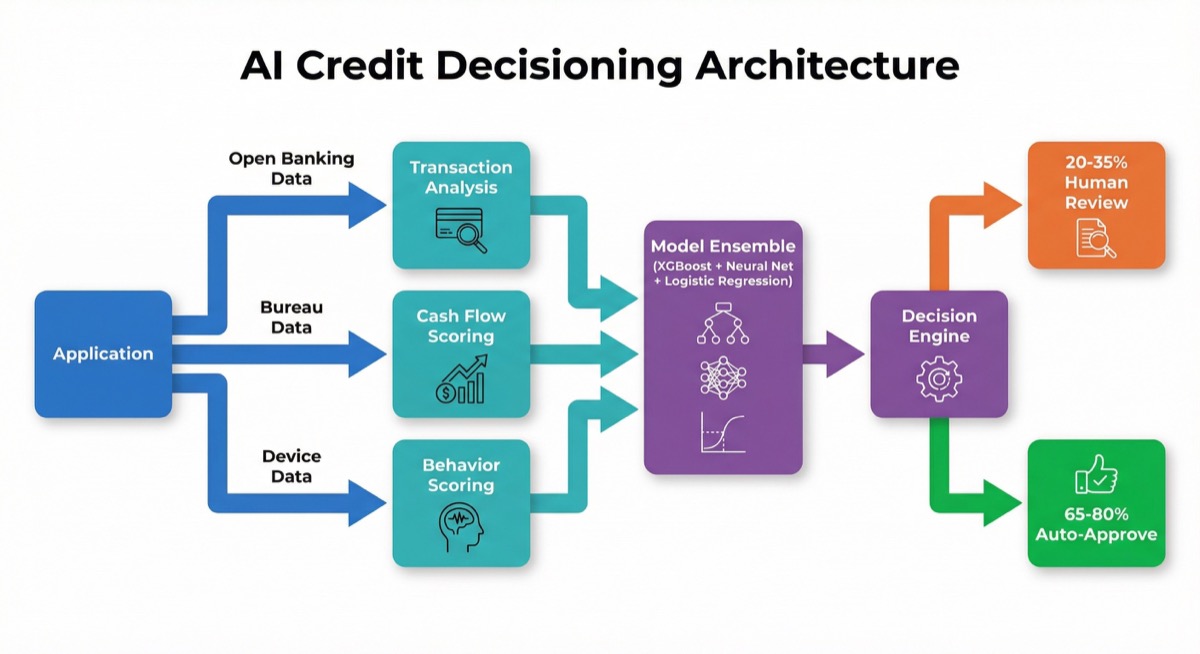

Alternative Data Credit Scoring:

- Bank transaction history analysis (cash flow patterns, income stability, spending behavior)

- Open banking data (with customer consent) for real-time financial health assessment

- Behavioral data from application process (time spent, corrections, device)

Instant Decision Engine:

- Pre-trained models that score applications in <2 seconds

- Confidence-based routing: high confidence → auto-approve/deny, low confidence → human review

- Continuous learning from loan performance data

Dynamic Pricing:

- Risk-adjusted interest rates calculated per application

- Real-time market condition integration

- Portfolio-level optimization (balancing risk appetite with growth targets)

Architecture Pattern

Measured Impact

| Metric | Traditional | AI-Powered | Change |

|---|---|---|---|

| Decision time | 1-5 days | <2 seconds | 99.9% faster |

| Auto-decision rate | 20-40% | 65-80% | 2-3x improvement |

| Default rate | Baseline | -15-25% | Better risk selection |

| Approval rate | Baseline | +10-20% | More creditworthy borrowers captured |

| Cost per decision | €15-30 | €2-5 | 80% reduction |

Application 4: Agentic AI for Operations

What's New in 2026

Agentic AI — autonomous AI systems that can plan, execute, and adapt multi-step workflows — is the frontier application in financial infrastructure. Unlike traditional ML models that score or classify, agentic systems take actions.

Production Use Cases (Today)

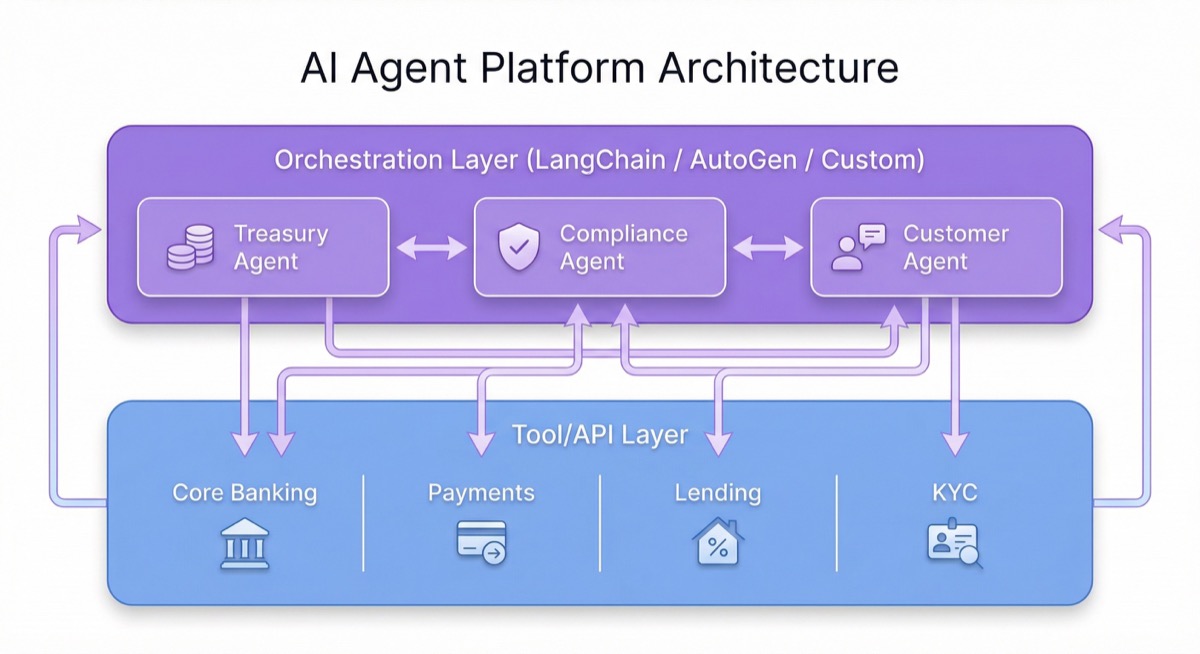

1. Intelligent Treasury Management

- AI agent monitors liquidity positions across accounts, currencies, and counterparties

- Automatically executes sweeps, placements, and FX hedges within pre-set parameters

- Escalates to human treasury manager for decisions exceeding risk limits

2. Automated Regulatory Reporting

- Agent collects data from multiple systems (core banking, payments, lending)

- Generates regulatory reports in required formats

- Validates completeness, flags anomalies, and submits on schedule

- Handles regulator queries by pulling supporting documentation

3. Customer Service Orchestration

- AI agent handles account inquiries, transaction disputes, and product questions

- Accesses core banking APIs to retrieve real data (not hallucinated responses)

- Escalates complex cases to human agents with full context summary

- Processes routine requests end-to-end (address changes, card replacements, statement generation)

4. Reconciliation and Exception Handling

- Agent monitors settlement and reconciliation queues

- Automatically investigates and resolves standard exceptions (timing differences, format mismatches)

- Creates investigation tickets for genuine discrepancies with preliminary root cause analysis

Architecture: The AI Agent Platform

The Critical Guardrails

Agentic AI in financial services requires strict boundaries:

- Action limits: Maximum transaction amounts an agent can execute without human approval

- Audit trails: Every action logged with reasoning chain

- Kill switches: Immediate human override at any point

- Regulatory compliance: Agent actions must comply with all applicable regulations

- Testing: Extensive simulation before production deployment

ROI Projection

For a financial institution with 200K accounts:

- Treasury management automation: €80-150K/year (1-2 FTE equivalent)

- Regulatory reporting automation: €60-120K/year (reduced errors + staff time)

- Customer service automation (60% deflection): €150-300K/year (3-5 FTE equivalent)

- Reconciliation automation: €40-80K/year (1 FTE + faster resolution)

- Total: €330-650K/year

Implementation Roadmap

Phase 1: Foundation (Months 1-6)

- Implement real-time fraud scoring (highest immediate ROI)

- Deploy compliance alert triage

- Build feature store and ML infrastructure

- Investment: €200-400K | Expected ROI: €300-500K/year

Phase 2: Expansion (Months 6-12)

- Launch AI credit decisioning

- Implement SAR generation assistance

- Dynamic customer risk scoring

- Investment: €150-300K | Expected ROI: €400-700K/year

Phase 3: Agentic (Months 12-24)

- Deploy treasury management agent

- Launch customer service AI

- Automated regulatory reporting

- Investment: €200-400K | Expected ROI: €300-600K/year

Cumulative 2-year investment: €550K-1.1M Cumulative annual ROI by year 2: €1.0-1.8M/year

The Platform Requirement

AI in financial infrastructure isn't a standalone product — it's a capability layer that sits on top of core banking. The platform must provide:

- Real-time event streams (every transaction, every state change)

- Rich APIs for AI agents to query and act

- Structured audit trails for regulatory compliance

- Feature store integration for ML model serving

- Granular permissions for AI agent actions

CoreFi's API-first architecture provides all of these as native capabilities, making AI integration a configuration exercise rather than a development project.

Ready to move beyond AI buzzwords? CoreFi's modular platform provides the API-first foundation for production AI in financial services — from fraud detection to agentic operations. Schedule a technical deep-dive with our team.

![Cloud-Native, Agentic, Compliant-by-Design — In That Order [2026 CEO View] | CoreFi](/assets/images/articles/cloud-native-agentic-compliant-by-design-hero.svg)

![Multi-Tenant vs Single-Tenant Core Banking — Regulator Questions [2026] | CoreFi](/assets/images/articles/multi-tenant-vs-single-tenant-what-regulators-ask-hero.svg)

![Lending Lifecycle Automation — Where Humans Still Belong [2026] | CoreFi](/assets/images/articles/lending-lifecycle-automation-where-humans-still-belong-hero.svg)