Multi-Jurisdiction EU Fintech Deployment: Licensing, GDPR & Passporting [2026] - CoreFi

CoreFi · 11 min read

![Multi-Jurisdiction EU Fintech Deployment: Licensing, GDPR & Passporting [2026] - CoreFi](/wp-content/uploads/2024/11/2.png)

Everyone in fintech talks about "scaling across Europe." The pitch deck says "EU-wide passporting." The reality involves 27 different tax authorities, 22 different languages, conflicting regulatory interpretations, and GDPR data residency requirements that vary by country.

We know because we've done it. CoreFi operates in Italy and Spain, with the regulatory groundwork laid for EU-wide expansion. This article shares what we've learned — the stuff that isn't in any vendor's marketing materials.

The Passporting Promise vs. Reality

How Passporting Is Supposed to Work

The EU single market provides "passporting" — a license obtained in one member state is valid across all 27. This applies to:

- CRD/CRR (banking license): Passport via home state NCA notification

- PSD2/PSD3 (payment institution): Passport via home state NCA

- EMD2 (e-money institution): Passport via home state NCA

- ECSPR (crowdfunding): Passport via home state NCA (CNMV for Spain, CONSOB for Italy)

- MiCA (CASP): Passport via home state NCA

How It Actually Works

Step 1: Get your home license. This takes 6-18 months depending on jurisdiction and license type. CNMV (Spain) processes ECSPR applications in 3-6 months. BaFin (Germany) can take 12-18 months.

Step 2: Notify host state NCAs. Your home NCA sends a notification to every country where you want to operate. Legally, the host NCA has 3 months to respond (or it's automatic).

Step 3: Wait for reality to set in. Host NCAs often:

- Request additional documentation beyond what the directive requires

- Impose local conduct-of-business rules that effectively create new requirements

- Take longer than 3 months to respond, with limited accountability

- Require local language documentation for consumer-facing products

The honest timeline:

- Home license: 6-18 months

- First passport (1 country): 3-6 months

- Full EU coverage (5+ countries): 12-24 months of rolling notifications

Jurisdiction Selection Strategy

Not all EU countries are equal for fintech licensing. Here's a practical ranking:

Tier 1 — Fast, fintech-friendly:

- 🇱🇹 Lithuania: Fastest EMI/PI licensing in Europe (3-6 months), English-language process, low capital requirements

- 🇪🇸 Spain (CNMV): Strong for ECSPR/crowdfunding, reasonable timelines, growing fintech ecosystem

- 🇮🇪 Ireland (CBI): English-language, access to both EU and UK-adjacent market

- 🇳🇱 Netherlands (DNB): Pragmatic regulator, strong payments ecosystem

Tier 2 — Solid but slower:

- 🇫🇷 France (ACPR/AMF): Large market, thorough review process, French language required

- 🇩🇪 Germany (BaFin): Largest EU market, but slow and demanding licensing process

- 🇮🇹 Italy (Banca d'Italia/CONSOB): Growing fintech regulation, dual oversight can be complex

Tier 3 — Specialized:

- 🇱🇺 Luxembourg (CSSF): Fund management, investment services

- 🇪🇪 Estonia: Digital-first, but recent tightening of crypto licensing

- 🇲🇹 Malta: Historically crypto-friendly, small market

Data Residency: The GDPR Minefield

The Base Rule

GDPR allows personal data to flow freely within the EEA. In theory, you can process Italian customer data in a data center in Ireland.

The Real Complications

1. Banking Secrecy Laws

Several EU countries have additional banking secrecy requirements that go beyond GDPR:

- Luxembourg: Banking secrecy law (Loi du 5 avril 1993) requires enhanced confidentiality controls

- Austria: Traditional banking secrecy, relaxed but still relevant

- Germany: Strict data minimization enforcement by state-level DPAs

2. NCA Data Access Requirements

National regulators often require that customer data be accessible from within their jurisdiction:

- Transaction records must be producible within specific timeframes (often 24-48 hours)

- Some NCAs require dedicated database access or local reporting servers

- Audit data must be available in local language

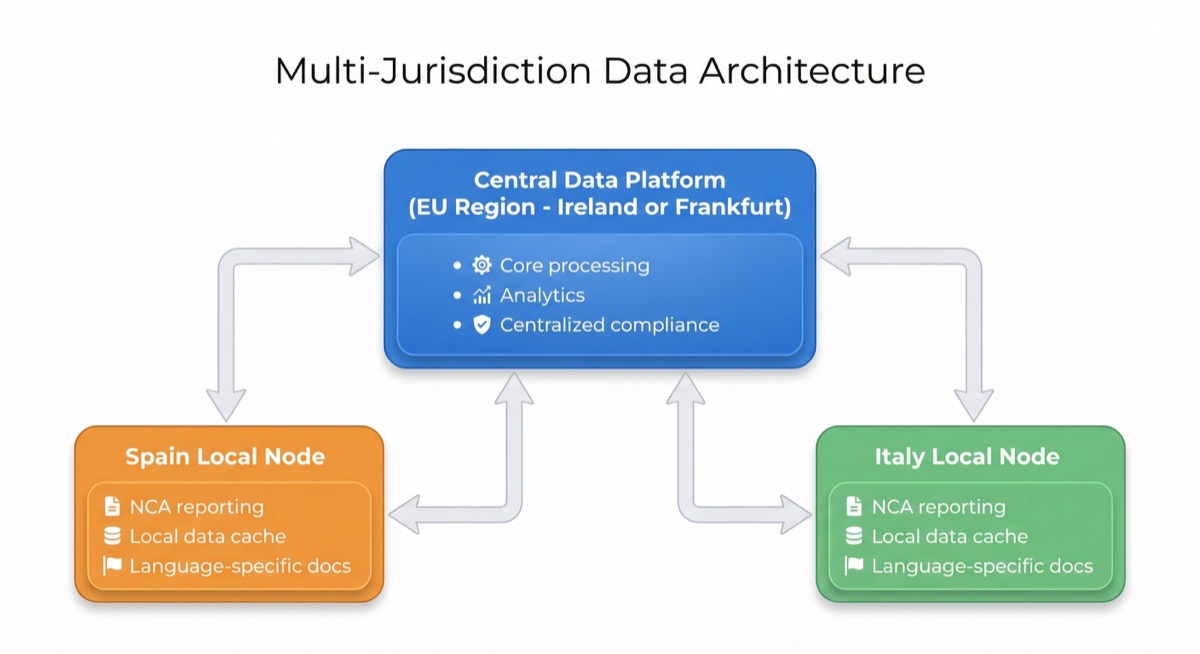

3. The Practical Architecture

Most multi-jurisdiction fintechs end up with a hub-and-spoke data architecture:

Cost implication: Each local node adds €20-50K/year in infrastructure and €10-20K/year in maintenance. For 5 countries, that's €150-350K/year just for data architecture.

Tax Reporting: The Nightmare Nobody Mentions

What's Required

Every EU country has different tax reporting requirements for financial institutions:

- Italy: Withholding tax on interest income (26%), annual CRS reporting to Agenzia delle Entrate, FATCA reporting

- Spain: Modelo 196 (account information), Modelo 291 (non-resident reporting), CRS/FATCA

- Germany: KapSt (capital gains tax withholding), Freistellungsauftrag (tax exemption orders), annual reporting to BZSt

- France: IFU (Imprimé Fiscal Unique) for investment income, prélèvement forfaitaire unique (30% flat tax)

The Technical Burden

Each country's tax reporting requires:

- Different data formats and schemas

- Different submission protocols (XML, XBRL, CSV, API)

- Different deadlines and correction procedures

- Different handling of cross-border situations (double taxation treaties)

Engineering cost: Building and maintaining tax reporting for each new jurisdiction costs €40-80K in initial development plus €15-30K/year in maintenance (schema changes, regulatory updates).

CRS/FATCA: The Universal Layer

The Common Reporting Standard (CRS) and FATCA (for US persons) apply everywhere, but each country has its own submission format and portal:

- XML schema varies by country (some follow OECD standard, some add national extensions)

- Submission portals are country-specific

- Error handling and correction procedures differ

- Due diligence requirements have national variations

Language and Localization

Legal Requirements

Consumer-facing financial products in the EU must be provided in the local language. This isn't optional — it's a regulatory requirement in most jurisdictions:

- Pre-contractual information: Must be in the customer's language

- Terms and conditions: Local language required

- Complaints handling: Must accept and respond in local language

- Regulatory disclosures: Local language required

What This Means Technically

For each new jurisdiction, you need:

- Full UI/UX translation (not just Google Translate — financial terminology requires specialized translators)

- Legal document translation and review by local counsel

- Customer support in local language (or at minimum, English + local)

- Marketing materials and onboarding flows in local language

- Local payment method support (Bizum in Spain, Bancomat in Italy, iDEAL in Netherlands)

Cost per language: €30-60K initial translation + €10-20K/year for maintenance and new content.

The Real Multi-Jurisdiction Playbook

Based on our experience expanding from Italy to Spain, here's the practical sequence:

Phase 1: Home Market (Months 1-12)

- Obtain home license

- Build core platform with multi-jurisdiction architecture from day one

- Implement CRS/FATCA reporting

- Launch in home market

- Cost: Already in your core build budget

Phase 2: First Expansion (Months 12-18)

- Passport to first target market

- Set up local compliance node

- Implement local tax reporting

- Translate UI, legal docs, and support

- Local payment method integration

- Cost: €150-300K

Phase 3: Scaling (Months 18-36)

- Passport to 3-5 additional markets simultaneously

- Template-based deployment (each new market is faster)

- Centralize where possible, localize where required

- Cost per additional market: €80-150K (decreasing with scale)

Phase 4: Full EU Coverage (Months 36-48)

- Remaining markets (often smaller, less complex)

- By this point, your architecture handles new markets in 4-8 weeks

- Cost per additional market: €40-80K

Lessons Learned

1. Build multi-tenant from day one. Retrofitting multi-jurisdiction support into a single-tenant architecture costs 5-10x more than building it in.

2. Pick your licensing jurisdiction carefully. Your home license jurisdiction determines your primary regulator forever. Choose based on speed, language, and regulatory culture.

3. Budget for local counsel in every market. Remote legal advice doesn't work for financial regulations. You need local lawyers who know the NCA personally. Budget €20-40K per country per year.

4. Tax reporting is the bottleneck. Licensing and passporting get all the attention, but tax reporting integration is consistently the most time-consuming technical challenge.

5. Don't underestimate localization. Financial products in English only will fail in continental Europe. Users expect their banking language to be their language.

CoreFi's platform is built for multi-jurisdiction deployment from the ground up — with native support for EU regulatory frameworks, multi-language interfaces, and country-specific compliance modules. Currently live in Italy and Spain. Talk to us about expanding your financial services across Europe.

![Cloud-Native, Agentic, Compliant-by-Design — In That Order [2026 CEO View] | CoreFi](/assets/images/articles/cloud-native-agentic-compliant-by-design-hero.svg)

![Multi-Tenant vs Single-Tenant Core Banking — Regulator Questions [2026] | CoreFi](/assets/images/articles/multi-tenant-vs-single-tenant-what-regulators-ask-hero.svg)

![Lending Lifecycle Automation — Where Humans Still Belong [2026] | CoreFi](/assets/images/articles/lending-lifecycle-automation-where-humans-still-belong-hero.svg)